Dubai’s property market continued its record-breaking run through Q3 2025, defying the usual summer slowdown. Transaction volumes in July and August reached historic highs, prices climbed further above previous peaks, and investor demand remained robust across residential and commercial segments. Below, we provide a detailed overview of market performance in July, August, and early September 2025, highlight the top developers and major project handovers, examine trends in both residential and commercial sectors (including price hotspots), and analyze rental market dynamics and yields. Charts and tables summarizing key data – such as top developers by sales, area-wise price changes, and transaction volumes – are included to visualize the trends. All data is drawn from reputable sources including the Dubai Land Department (DLD), leading portals (Bayut, Property Finder), and industry reports by CBRE, Knight Frank, and others.

Frequently Asked Questions (FAQ)

Overall Market Performance (Q3 2025)?

The Dubai Real Estate Market continued a record-breaking run in Q3 2025, defying the usual summer slowdown. Transaction volumes in July and August reached historic highs (July logged over 20,000 sales transactions), prices climbed further, and investor demand remained robust across residential and commercial sectors. The quarter delivered one of the “busiest summers on record,” driven by strong off-plan sales and sustained investor confidence.

Top Performing Developers?

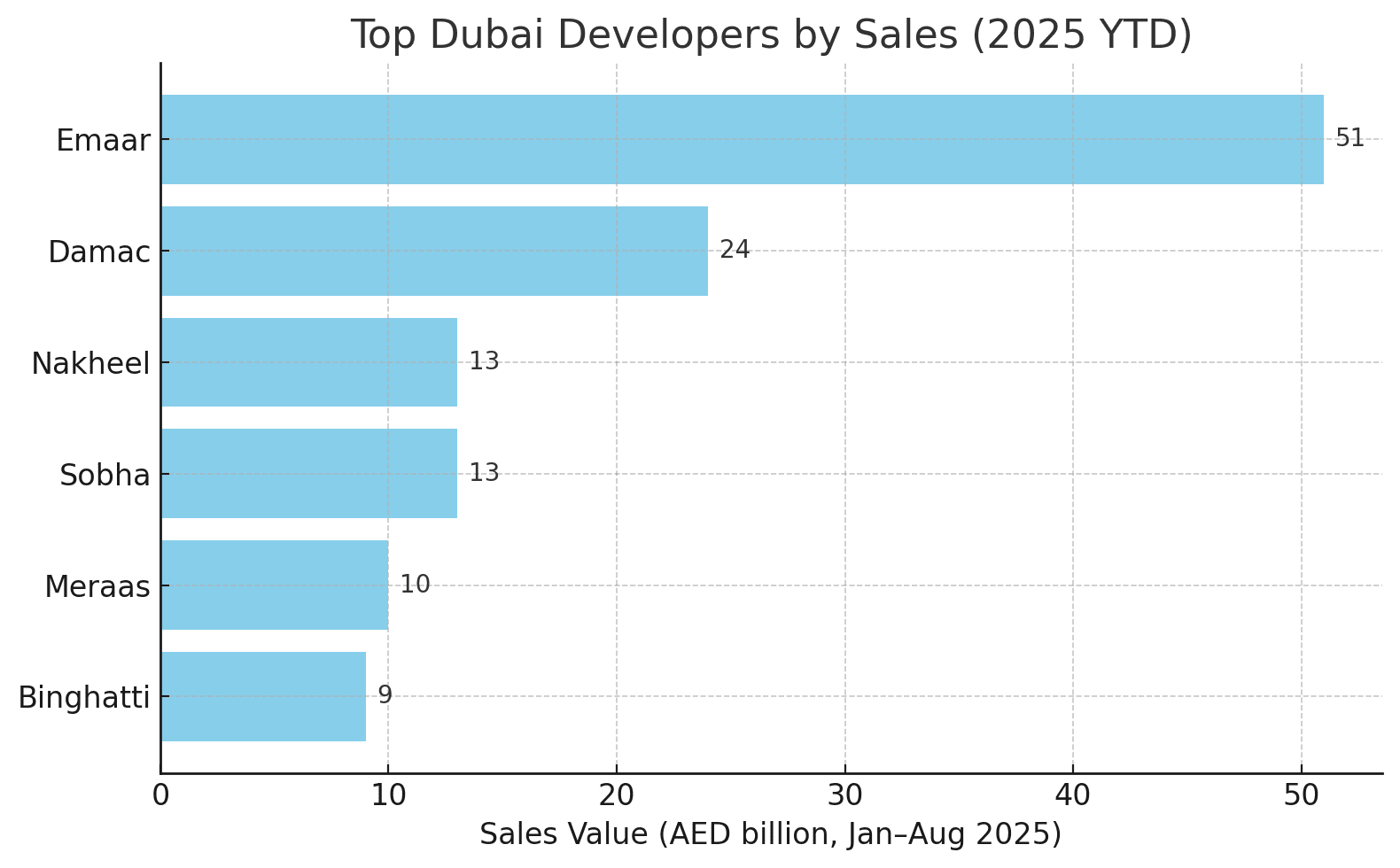

Emaar Properties solidified its position as the top-performing developer, achieving roughly AED 51 billion in property sales (approx. 10,000 transactions) year-to-date up to August 2025. DAMAC Properties was the second-place leader with about AED 24 billion in sales, followed by Nakheel, Sobha Realty, and Meraas.

Key Residential Price Trends?

Villa and townhouse properties continued to see the most robust appreciation due to limited ready supply and persistent end-user demand, with many prime villa communities seeing prices 10%–20% higher year-on-year. Apartment price growth, while still positive, began to moderate in some established communities, although high-demand areas like Jumeirah Village Circle (JVC) still saw strong annual gains (around +17% YoY).

Dubai Rental Market Performance?

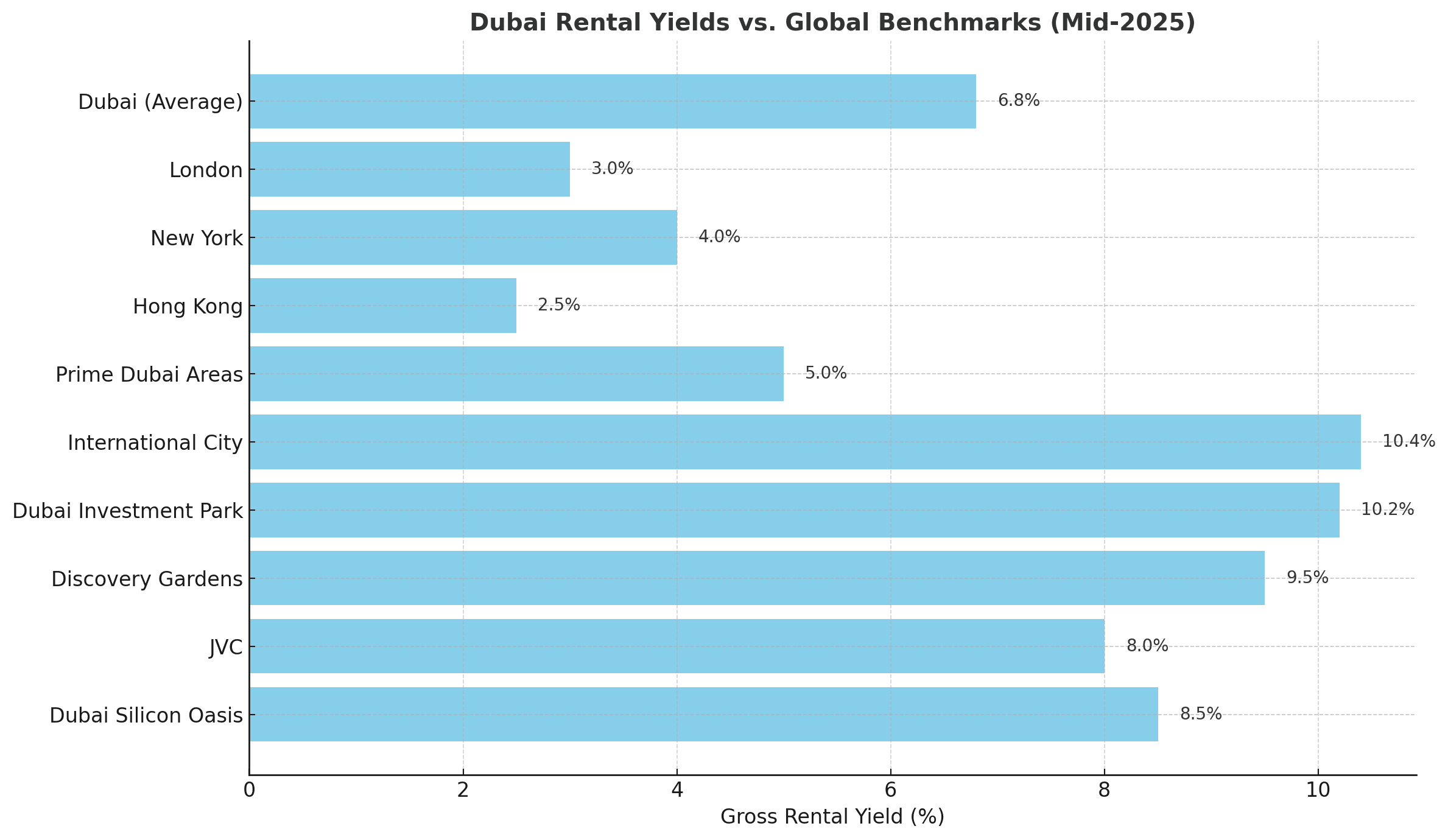

The rental market remained strong, but the rate of rent increases decelerated compared to previous years due to the influx of new supply. The annual rental growth rate dropped to about 8.5% by mid-2025. Despite this cooling, Dubai’s average gross rental yield remained highly attractive at around 6.8% in mid-2025, with high-yielding locations like International City and Dubai Investment Park offering returns of 9%–10%.

Off-Plan vs. Ready Properties Dominance?

Off-plan (new development) sales were highly dominant in Q3 2025, comprising roughly 65%–72% of all residential sales during the summer months. This was fueled by developers’ generous payment plans and a high volume of new project launches in areas like Jumeirah Village Circle and Business Bay.

Dubai’s property market continued its record-breaking run through Q3 2025, defying the usual summer slowdown. Transaction volumes in July and August reached historic highs, prices climbed further above previous peaks, and investor demand remained robust across residential and commercial segments. Below, we provide a detailed overview of market performance in July, August, and early September 2025, highlight the top developers and major project handovers, examine trends in both residential and commercial sectors (including price hotspots), and analyze rental market dynamics and yields. Charts and tables summarizing key data – such as top developers by sales, area-wise price changes, and transaction volumes – are included to visualize the trends. All data is drawn from reputable sources including the Dubai Land Department (DLD), leading portals (Bayut, Property Finder), and industry reports by CBRE, Knight Frank, and others.

Market Performance Overview (July to September 2025)

Record Transaction Volumes and Sustained Growth: The period from July to September 2025 saw Dubai real estate transactions surge to some of their highest levels on record. July 2025 logged over 20,000 sales transactions, a +24–25% increase year-on-year, marking the second-highest monthly volume ever[1][2]. This followed a slight dip in June (due to Eid holidays) and represented a strong normalization of activity[3]. Total sales value in July exceeded AED 65 billion, up around 30% from July 2024[2]. Average property prices hit new highs, reaching about AED 1,625 per square foot – 31% above the last market peak in 2014[4].

August 2025 maintained the momentum with 18,678 real estate deals worth AED 51.1 billion, registering a +15.4% jump in volume and +7.9% in value year-on-year[5][6]. In fact, August 2025 was the highest on record for that month, only slightly below July’s peak. Apartments led the charge (over 15,900 apartment sales in August, +29.2% YoY) while villa transactions were fewer (1,944 sales, –38% YoY) due to limited ready supply[7][8]. Nonetheless, the average villa price per square foot rose ~15% YoY to AED 1,720, reflecting sustained demand for quality villas[8]. Commercial property and land sales also grew steadily, with commercial deals up ~20% YoY (442 transactions, ~AED 1.2B in August) and plot sales up 7% (392 transactions, ~AED 8.9B)[9]. These figures underscore that Dubai’s market defied the usual summer lull, delivering one of the busiest summers on record[10].

September 2025 data was still being finalized at the time of writing. However, early indicators suggest that Q3 closed out strongly, continuing the pattern of high transaction volumes and price resilience. Market observers note that buyer demand remained “highly positive” heading into autumn, even if a slight seasonal pause was expected[11]. Year-to-date (YTD) sales by early September surpassed 140,000 transactions, more than 20% higher than the same period in 2024, keeping Dubai on track to exceed 200,000 sales transactions in 2025 – an all-time high[12]. This exceptional performance reflects Dubai’s robust economic fundamentals, population growth, and investor confidence, which have so far outweighed concerns about oversupply or summer slowdowns.

Top Developers & Major Project Handovers (Q3 2025)

Market Leaders in Sales: A handful of major developers drove a large share of sales in July–Sep 2025. Emaar Properties solidified its position as the top-performing developer – between January and August 2025, Emaar achieved roughly AED 51 billion in property sales (around 10,000 transactions)[13]. This was nearly double the sales of the second-place developer, DAMAC Properties, which recorded about AED 24 billion in sales (~9,000 transactions)[13]. Other leading developers during this period included Nakheel (≈AED 13B), Sobha Realty (≈AED 13B), and Meraas (~AED 10B)[13]. Up-and-coming private developers also made their mark – for example, Binghatti Developers (known for mid-market projects) notched roughly AED 9B in sales (~6,000 deals), while Aldar Properties (expanding from Abu Dhabi into Dubai) saw about AED 8B in sales (~1,700 deals) by August[14]. The chart below illustrates the top developers by sales value in 2025 year-to-date:

Top Dubai developers by total sales value (AED billion) in 2025 up to August[13][15]. Emaar and DAMAC lead by a wide margin, followed by Nakheel, Sobha, Meraas, and others.

This concentrated success of major developers is underpinned by Dubai’s influx of buyers (both local and foreign) seeking properties from reputed names. Emaar’s sales, for instance, jumped 46% year-on-year in H1 2025, reaching AED 46B thanks to robust off-plan demand and iconic projects[16]. Similarly, Damac’s branded luxury offerings and new community launches (e.g. Lagoon-themed villas) attracted strong uptake. Sobha Realty benefited from its reputation for high-quality finishes in projects like Sobha Hartland, while Nakheel capitalized on its famed waterfront communities (Palm Jumeirah, etc.), and Meraas/Dubai Holding saw sales in destinations like City Walk, Bluewaters, and new villa enclaves.

Major Project Completions (Jul–Sep 2025): The third quarter of 2025 also witnessed significant project handovers, adding new supply to the market – especially in the prime segment. Notably, Emaar delivered the Address Residences Dubai Opera in Downtown Dubai in Q3 2025, a twin-tower branded residence complex near the Opera House[17]. This high-profile handover has introduced new ultra-luxury apartments in the Downtown district, catering to unabated demand for prime city-center homes. Meraas (Dubai Holding) completed the Bluewaters Bay Residences on Bluewaters Island (Q3 2025)[18], expanding the stock of seafront apartments with views of Ain Dubai and the Dubai skyline. These deliveries in Downtown and Bluewaters mark milestones, as they bring hundreds of ready units to market and cater to buyers seeking turnkey luxury properties in Dubai’s most desirable locations.

Several master-developer communities saw phases handed over during this period as well. At DAMAC Lagoons, one of the themed villa clusters (e.g. Portofino) was slated for handover by Q3 2025[19], adding to the inventory of family villas around the man-made lagoons. In Emaar’s suburban projects, phases in Arabian Ranches III and Emaar South continued to complete on schedule, while The Valley (Talia cluster) moved closer to handover towards late 2025[19]. The sheer scale of deliveries underscores the supply boom underway: in H1 2025 alone, over 20,000 new residential units were delivered (with 90,000+ units expected for full-year 2025) according to Betterhomes data[20][21]. Key delivery hotspots include Jumeirah Village Circle (accounting for ~20% of H1 deliveries), Sobha Hartland (11%), and Mohammed Bin Rashid City (8%)[22] – areas where multiple projects reached completion, offering buyers more options and potentially easing price pressure on rentals.

Implications: The dominance of top developers in sales shows buyers’ preference for established brands with a track record of delivery. These developers are also leading the charge in new launches (for example, Emaar’s “Rosehill” towers in Dubai Hills launched in Q3[23], and Nakheel’s Nad Al Sheba Gardens Phase 10 launch[24]), ensuring a pipeline of future supply. The wave of project handovers in 2025, particularly in emerging communities, is gradually shifting Dubai toward a more supply-balanced market, which could stabilize rents and prices in the mid-term[25]. In the short term, however, the successful absorption of these new units in Q3 indicates that demand – both investor and end-user – has remained strong enough to keep up with the increased supply, at least in popular locations.

Residential vs. Commercial Property Trends

Residential Segment – Off-Plan Dominance and Villa Demand: Dubai’s residential market in Q3 2025 was characterized by continued strength in off-plan (new development) sales and a two-tier dynamic between apartments and villas. Off-plan transactions comprised roughly 65%–72% of all sales during the summer months, as developers’ generous payment plans and new project launches attracted buyers[26][10]. In July, off-plan (or “Oqood”) deals jumped 34% YoY in volume and 46% in value[27], and by August off-plan’s share of sales had reached about 72% of all deals – a reflection of many buyers favoring newly launched units over the resale market[28]. This surge in off-plan activity was led by high-profile launches in areas like Jumeirah Village Circle and Business Bay, which were the top two neighborhoods for first-time sales in Q3[29][30]. Developers brought over 13,800 new residential units to market in July alone (50+ project launches) and nearly 93,000 units year-to-date by end of July, an unprecedented pace of new supply injection[31][32]. While such volume might suggest risk of oversupply, market observers note that buyer appetite remained resilient; however, projects that once sold out in hours are now taking longer to fully book, indicating that buyers have become more selective and value-focused amid the plethora of choices[33].

Within the residential space, apartments vs. villas showed diverging trends. Apartments formed the bulk of transactions (over 80% of sales by unit count)[34], and price growth for apartments has begun to moderate in some established communities[35]. For example, the Property Monitor index showed apartment price growth softening to under +1% monthly by July[4]. Many affordable-to-mid tier apartment areas still notched steady gains (3–10% price rises in H1 2025)[36], but the top-tier apartment districts (Downtown, Marina, Palm Jumeirah) are closer to price plateaus, having surpassed their last peak values. By contrast, villas and townhouses continued to see robust appreciation due to limited ready supply and persistent end-user demand. In many prime villa communities, prices were 10–20% higher than a year ago by mid-2025[37]. For instance, Arabian Ranches and Dubai Hills Estate saw villa resale prices around 20% higher year-on-year, and even some new villa suburbs like Tilal Al Ghaf and Jumeirah Golf Estates were up ~15–22% YoY[37]. This trend was evident even in Q3: fewer villa sales took place in August (–38% YoY in volume) due to scarce inventory, yet buyers paid significantly more per unit, driving the average villa price/sqft up by 15% from a year prior[8]. In summary, villas remained the hottest commodity, with price growth far outpacing apartments, whereas apartment sales volume was high but price increases were more modest overall.

Commercial & Land Segment – Broad-Based Uptick: Dubai’s commercial real estate sector quietly gained momentum over the summer as well. Office and retail property transactions, while a small fraction of total sales, showed strong growth signs. August saw 442 commercial property sales worth AED 1.2B, a 20%+ increase in deal count year-on-year[9]. Businesses are expanding and new investors are entering the office market, drawn by Dubai’s economic growth and relatively higher yields in commercial assets. There were even reports of exceptional spikes – for example, one analysis noted the average price of commercial rentals had “skyrocketed by 200%” year-on-year in July[38] – although such a figure likely reflects select high-end leases rather than the entire market. In general, office rents have been rising in prime areas due to low vacancy, and this has started translating into higher capital values and sales activity for offices/warehouses in hubs like Business Bay, JLT, and Dubai Investments Park.

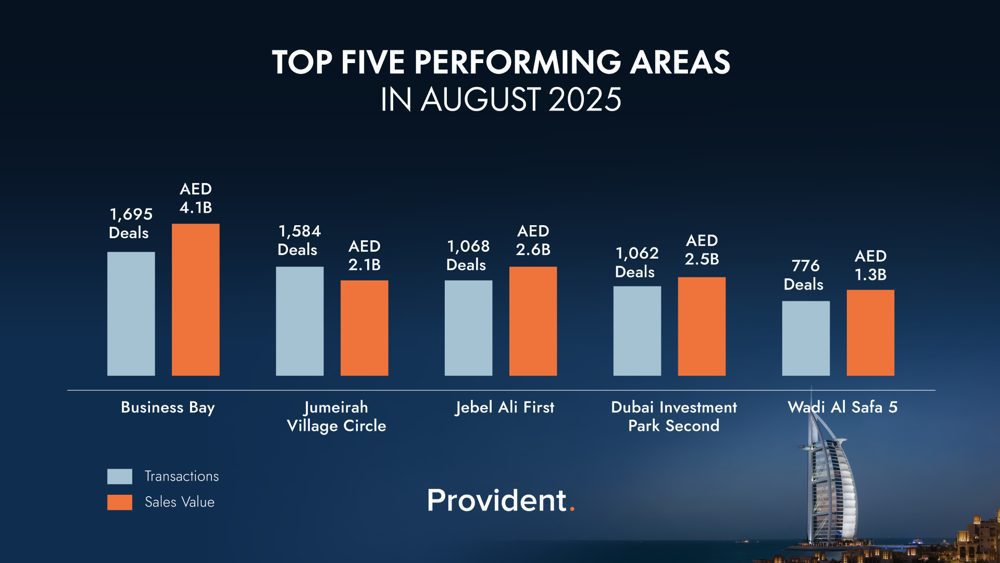

The land (plots) segment also performed well, appealing to both developers and long-term investors. In August, 392 plot sales totaling AED 8.9B were recorded (+7.4% YoY)[7], continuing a trend of strong land acquisitions seen in H1. DLD data for H1 2025 showed Al Yalayis 1, Wadi Al Safa 5, and Al Barsha South Fourth – areas with large master developments – among the top locations by transaction volume[39], driven largely by bulk land sales for new projects. Notably, Al Barsha South Fourth (Arjan area) topped H1 rankings with 10,469 transactions[40], as several affordable apartment projects launched and transacted there. Business Bay and Dubai Marina led in transaction value in H1 (AED 22.5B and 25.1B respectively)[41], reflecting big-ticket deals (commercial towers, bulk unit sales) in those locales. Overall, the breadth of growth – across residential, commercial, and land – in Q3 shows a healthy diversification of investor interest, not just speculative flipping. The chart below highlights the top five areas by sales transactions in August 2025, illustrating how both established and emerging locations contributed to volume:

Top five performing areas in Dubai by number of sales transactions in August 2025[29]. Business Bay and Jumeirah Village Circle led activity, followed by Jebel Ali First (largely off-plan in Expo City Dubai), Dubai Investment Park Second, and Wadi Al Safa 5.

Property Price Trends & Hotspots

Despite the huge supply influx, prices in most segments continued their upward trajectory in Q3 2025, though with varying intensity across areas. Citywide average prices crept up through the quarter – e.g., +0.99% month-on-month in July[4] – bringing year-to-date gains into high single digits. However, the highest price increases were concentrated in specific “hotspot” neighborhoods:

- Prime Luxury Areas: Dubai’s top-end districts saw the most dramatic annual price jumps. Palm Jumeirah and Dubai Hills Estate stood out, with apartment prices approximately 15–20% higher in mid-2025 compared to a year earlier[42]. These areas benefited from ultra-wealthy buyer demand and limited new supply of similar caliber (especially for ready villas). Similarly, Emirates Hills and Jumeirah Bay Island (notably for villas) saw double-digit growth, as did high-end villa enclaves like Jumeirah Golf Estates (+22% YoY)[37]. Even within the prime segment, some niche communities achieved extraordinary appreciation – for example, Victory Heights (a villa community in Dubai Sports City) saw prices surge nearly 39% year-on-year[37], the result of a small inventory of villas there trading at a premium as families competed for available stock.

- Emerging and Mid-tier Areas: Mid-market communities generally experienced moderate price rises, though certain ones with new infrastructure or popularity spikes recorded notable gains. Jumeirah Village Triangle (JVT), for instance, was reported to have over 35% YoY growth in apartment prices (partly due to new, pricier projects entering the index)[35]. Jumeirah Village Circle (JVC) – one of the most active affordable areas – saw prices up around +17% YoY on average for apartments[43], reflecting its high demand from both investors and end-users. In the affordable apartment segment, locations like Dubai Silicon Oasis and International City saw modest increases (around 3–6% in H1 2025)[36][44], as a large pipeline of new units there kept prices competitive. Business Bay and Downtown Dubai apartments, having rebounded strongly in 2022–2023, were more stable by 2025 with single-digit annual growth (roughly 5–8% YoY)[43], indicating a mature equilibrium of supply and demand at the city-center.

- Areas with Price Corrections: It’s worth noting a few previously overheated locales did see minor price corrections or stabilization. For example, Palm Jumeirah’s villa segment (already at very high absolute price levels) showed only a +1.7% YoY increase by July[37], essentially flat, as some buyers balked at record villa prices there. Downtown Dubai’s ultra-luxury apartment prices also plateaued in Q3 after exponential growth in 2022–24. Overall, though, price declines were rare in Q3 2025, limited to isolated cases (e.g. a particular building or an overstretched sub-market). The broad trend was continued appreciation or stabilization at worst, as demand kept up with supply in most communities. Developers also strategically priced new launches to avoid undercutting the resale market, thereby supporting values.

In summary, Dubai’s price growth in Q3 2025 was led by the luxury and villa segment, while affordable apartments saw slower, sustainable gains. The steepest annual increases (15–20%+) were mostly in high-end neighborhoods and a few undersupplied villa enclaves[42]. More moderate rises (5–10% YoY) occurred in mainstream neighborhoods, and overall citywide prices are now significantly above pre-2020 levels. Industry consultants like CBRE and Knight Frank maintain an optimistic outlook, noting that resilient demand and proactive government policies have so far kept the market in growth mode, with the pace of price appreciation expected to gradually normalize rather than abruptly reverse[45].

Rental Market Trends and Yields

Rental Demand vs. New Supply: Dubai’s rental market in Q3 2025 remained strong, although signs of cooling emerged as new supply came online. The first half of 2025 saw 465,738 tenancy contracts registered (worth ~AED 42B), a slight increase in volume from the previous year[46]. This indicates that population growth (and tenant demand) is still absorbing new units. However, the rate of rent increases has decelerated compared to the frenetic growth of 2022–2023. According to market data, the annual rental growth rate in Dubai dropped to about 8.5% by mid-2025, down from ~14% at the start of the year[25]. By late Q3, many landlords found that rents in certain areas had reached an affordability ceiling, especially as thousands of newly completed apartments in areas like JVC, MBR City and Dubailand vied for tenants. Mid-market communities with abundant new deliveries (e.g. Dubailand suburbs, JVC) have seen rental rates stabilize and in some cases face slight downward pressure as tenants gain more choices[47][48]. On the other hand, prime districts (e.g. Palm Jumeirah, Dubai Hills, Downtown) continue to enjoy rental growth in the high single digits, fueled by wealthy expatriate inflows and relatively limited rental supply in those locales[49][50].

Rental Yields Remain Attractive: Despite slower rent growth, rental yields in Dubai remain among the highest of any global city, which sustained investor interest in Q3. The average gross rental yield across residential properties was around 6.8% in mid-2025[51], which is extremely competitive internationally. For context, yields in cities like London, New York, or Hong Kong are often only 2–5%. In Dubai, even prime areas often offer 4–6% yields, and the highest-yielding locations (typically affordable apartment districts) provide near double-digit returns. For example, investors could achieve approx. 9–10% rental yields in communities like International City, Dubai Investment Park, and Discovery Gardens[52][53]. Bayut’s H1 report showed International City apartments yielding about 10.4%, and DIP apartments around 10.2% annually[52][53]. Jumeirah Village Circle and Dubai Silicon Oasis also offered strong yields in the ~7–9% range, thanks to relatively low entry prices and steady rental demand[44][54]. These figures far outshine many mature markets – a fact not lost on global investors. In short, Dubai’s rental properties provide robust income streams, and this yield appeal has been a key driver of investment sales in Q3.

Tenant Buying Trend: Another interesting trend in the rental realm is the rise in tenants turning into homeowners, spurred by high rents and new residency incentives. Industry reports noted a “subtle but growing shift: more tenants are choosing to buy” in Dubai as of August[55]. With developers offering convenient payment plans and banks increasing mortgage lending, many long-term renters have found it financially sensible to purchase a home (especially with the prospect of locking in their housing costs and benefiting from capital appreciation). This trend was evidenced by the fact that 45% of new property investors in H1 2025 were UAE residents (tenants becoming owners)[56], a testament to initiatives aimed at converting tenants to buyers. As a result, while lease volume stays high, some demand is indeed shifting from rental to purchase – contributing to the strong sales figures we saw in Q3. It’s a positive sign of market maturation, though landlords in over-supplied areas may need to become more competitive on rents to retain tenants.

Outlook for Rents: Looking ahead, most analysts expect rent growth to continue slowing into late 2025, especially in the apartment segment, as the biggest wave of new deliveries in a decade hits the market[21]. Projections suggest that with ~90,000 new units completing in 2025 and another 120,000 in 2026[21], renters will have greater negotiating power, likely keeping rents flat or slightly lower in many mid-tier communities. Already in Q3, landlords started offering small discounts or added amenities to attract tenants in areas like Dubailand and JVC where multiple new buildings opened. However, for prime villas and established luxury districts, rents are forecast to hold firm or even rise further (albeit at a gentler pace) given the limited availability of such properties and ongoing interest from high-net-worth individuals. Overall, rental yields should remain healthy – even if rent growth cools, softer sales price growth in coming years could actually preserve or improve yields. As of 2025, yields of 7–8% in mid-market and 5% in prime are common, keeping Dubai on the radar for global investors chasing income-producing real estate[57].

Projects Delivered / Scheduled for Handover in Q3 2025

| Developer | Project / Community | Type | Status / Handover Notes |

|---|---|---|---|

| Emirates Properties | Azha Community (Al Amerah) | Villas community | Scheduled for handover in Q3 2025 with a 48/52 payment plan; starting prices ~ AED 1.74 million. Off Plan Projects+1 |

| Various / Master Communities | — | Residential Units city-wide | Prelaunch / analytics firms estimate ~37,000-42,000 residential units to be handed over in 2025; ~62% expected to be delivered on time. Key areas of handover include JVC, Dubai Hills Estate, Dubai South, Studio City, Sobha Hartland, JLT, Al Furjan. Off Plan Projects |

New Projects Announced / Launched in Q3 2025 (By Top Developers)

These may not yet be delivered, but were officially launched or announced in Q3 2025. Useful to mark what pipeline looks like.

| Developer | Project / Launch | Details |

|---|---|---|

| Emaar Properties | Rosehill at Dubai Hills Estate | Premium golf-facing twin towers, 1-3 bedroom apartments, flexible payment plan 80/20. Launched Q3 2025. artharealty.com |

| Binghatti Developers | Hillside at Dubai Science Park | Studios and 1-2 bedroom apartments near Al Barsha South, targeting investors. Prices (lower tier) from ~AED 675,000, handover expected in Q2 2026. artharealty.com |

| Nakheel | Nad Al Sheba Gardens Phase 10 | Mixed villas/townhouses (3 to 7 bedrooms). Family living, privacy, greenery. Completion projected by Q3 2027. artharealty.com |

Insights & Gaps

- The Azha Community by Emirates Properties is the clearest example of a project with handover in Q3 2025. It is a villa community, so this adds new ready-supply in the villa segment. Off Plan Projects

- The larger number of units handed over city-wide (37,000-42,000) suggests that many projects are completing or being delivered in 2025; however, only a portion of these deliveries are confirmed “on time.” Off Plan Projects

- Many of the new project launches will be delivered later (2026-2027+). So while supply is rising, only some portion was ready/handed over in Q3 2025.

- There is less publicly verifiable detail on exactly which projects beyond Azha have fully completed handover in July-September specifically.

Conclusion

Dubai’s real estate market from July to September 2025 demonstrated remarkable vitality, combining record transaction volumes with robust price growth and attractive investment returns. The summer months – traditionally slow – instead saw “one of the busiest summers on record” as Dubai defied seasonal trends[10]. Sales momentum was fueled by a high influx of new projects (off-plan sales hit historic levels) and sustained end-user demand for ready homes. Top developers like Emaar and DAMAC reaped the rewards, posting multi-billion-dirham sales and successfully launching new phases to meet demand[13]. The period also marked a transition toward greater supply: tens of thousands of new units were delivered or nearing completion, from Downtown penthouses to suburban villas, indicating Dubai’s commitment to growth. This expanding supply began to tame the once red-hot rental market, as rental growth eased to single digits – a welcome relief for tenants and a sign of a maturing sector[25].

As of Q3 2025, the market’s fundamentals appear strong. Buyer sentiment is buoyed by economic confidence, population gains, and government initiatives (golden visas, business-friendly policies). Prices are up year-on-year across almost all areas, yet analysts see a “soft landing” scenario rather than a sharp correction, thanks to high genuine demand and relatively controlled mortgage leverage. If anything, the moderation in price and rent growth is seen as stabilizing, preventing overheating while keeping Dubai property attractive versus global benchmarks. Yields of 6–8% are luring international investors seeking better returns than they can get in Europe or North America[57]. Meanwhile, end-users continue to find value, whether in the affordable segment (with many new affordable homes coming online) or in luxury (where Dubai still offers larger, newer prime properties at a fraction of London or New York prices).

In conclusion, Q3 2025 cements Dubai’s status as one of the world’s most dynamic real estate markets, where record-breaking growth and prudent sustainability are striking a careful balance. The stage is set for a strong finish to 2025: developers are gearing up for year-end launches, investors are eyeing high-profile events (like Expo City’s development) and tenants-turned-buyers are seizing opportunities in a market that remains fundamentally underscored by long-term confidence. As always, stakeholders will be watching supply indicators closely, but for now Dubai’s property sector is riding high on a wave of optimism, innovation, and enduring demand.

Sources: Dubai Land Department & Government Media Office[58][39]; Property Monitor (July 2025 Report)[1][35]; Property Finder insights; Bayut H1 2025 Market Report[36][52]; CBRE Research; Knight Frank Dubai Market Updates[25][42]; Provident & One Investments Market Reviews[5][59]; Skyline Holdings analysis[60][22]; Artha Realty and Prelaunch data[61][62]; Novvi Properties July report[2][43]; Engel & Völkers Snapshot[10][55]; Emaar PJSC H1 2025 Results[16].

[1] [11] [26] [27] [34] [35] [37] [51] July 2025 – Residential Market Report

https://a.storyblok.com/f/209096/x/7c6fac7bda/july-2025-residential-market-report.pdf

[2] [38] [43] Dubai Real Estate Report: July 2025 Market Trends & Data

https://www.novviproperties.com/blog/dubai-real-estate-market-report-july-2025

[3] [4] [12] [31] [32] [33] Monthly Market Report July 2025 – Property Monitor

https://propertymonitor.com/insights/monthly-market-report/monthly-market-report-july-2025

[5] [7] [29] [30] AED 51.1B property sales in Dubai August 2025 | Provident Estate

https://providentestate.com/blog/dubai-real-estate-sales-august-2025/

[6] [8] [9] [59] Dubai real estate hits Dh51.49 Billion in August sales – One Investments

https://oneinvestments.com/2025/09/07/dubai-real-estate-hits-dh51-1-billion-in-august-sales/

[10] [28] [55] Dubai Market Report & Insights – August 2025

https://www.engelvoelkers.com/ae/en/research/residential-market-snapshot-august-2025

[13] [14] [15] Top 10 Developers with Highest Sales in 2025 | Provident Estate

https://providentestate.com/blog/top-10-developers-with-highest-sales-in-2025/

[16] Emaar’s H1 2025 Property Sales increased 46% to reach ~AED 46 billion (US$ 12.5 billion); Backlog Increased by 62% to AED 146.3 billion (US$ 39.8 billion) | Emaar Properties

[17] [18] [61] [62] Dubai Property Handover Schedule 2025-2027: Completion Timeline Analysis | Best Off Plan Projects

https://prelaunch.ae/dubai-property-handover-schedule-2025-2027-completion-timeline-analysis/

[19] Top Real Estate Projects in Dubai Set for Handover in 2025

https://www.nextlevelrealestate.ae/top-real-estate-projects-in-dubai-set-for-handover-in-2025/

[20] [21] [22] [25] [42] [46] [47] [48] [49] [50] [60] Dubai Real Estate: 24 Projects Completed and AED 151B Residential Sales in H1 2025 – Will Rents Cool in H2? | Skyline Holdings

[23] [24] Top Dubai Developers and New Launches | Q3 2025 Update

[36] [44] [52] [53] [54] Bayut’s Dubai Sales Market Report H1 2025 – MyBayut

https://www.bayut.com/mybayut/dubai-sales-market-report-h1-2025/

[39] [40] [41] [56] [58] Dubai real estate transactions exceed AED431 billion in H1 2025

[45] UAE’s Residential Property Market Analysis 2025

https://www.globalpropertyguide.com/middle-east/united-arab-emirates/price-history

[57] Dubai real estate is outpacing the world in 2025. Prices are rising